While the blockage of the Suez Canal by the Ever Given in March was headline news all over the world, the current disruption in Yantian and surrounding ports is now on track to affect a larger volumes of containers, potentially for a longer time.

Analysis by Zencargo contributor Lars Jensen explains, ‘During the 14 days of Yantian port congestion, the port has been unable to handle approximately 357,000TEU, while Suez Canal blockage was impacting a daily flow of 55,000TEU for six days, which translates to a total of 330,000TEU.’

Today we look at the current situation in more depth, with specific numbers and shipments covered in the usual market update.

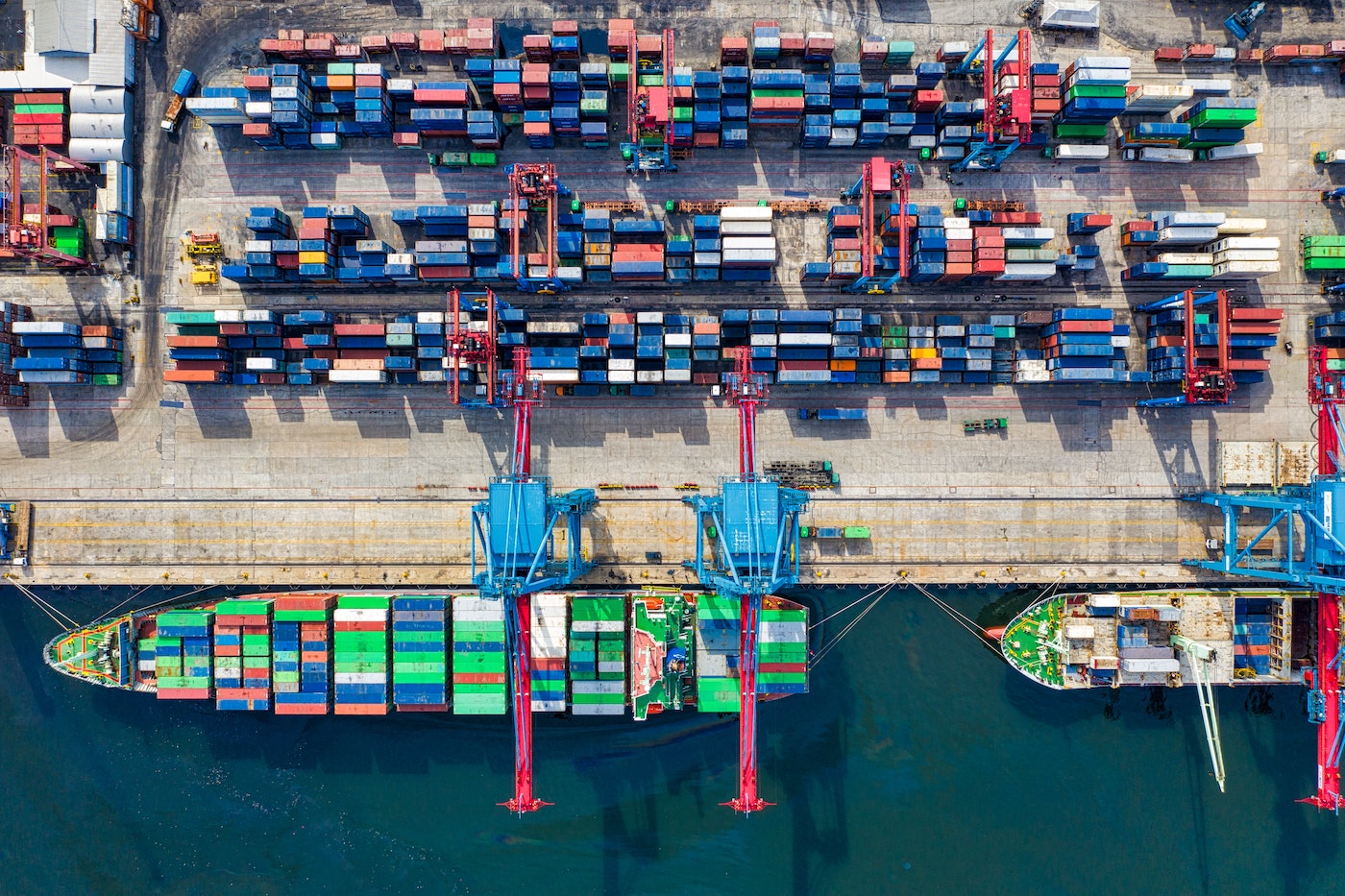

What’s going on in Yantian?

Disruption continues to spread through the ports of Yantian, Shekou and Nansha in the Greater China Area. The main reason for this is an increase in positive COVID-19 cases, which have been escalating in the last two weeks. Local authorities are responding with restricted operations and reduced staffing levels which has significantly lowered productivity at the ports.

Disinfection and quarantine measures have raised yard density at Yantian International Container Terminal (YICT).

Due to further measures being implemented, increased congestion and vessel delays upwards of 15 days are expected in Yantian port.

All operations in the western area of YICT have been suspended until further notice. Origin export containers and transshipment containers have been detained there until further notice.

Operation in the eastern area of the terminal where mother vessels mainly berth continues to experience the low productivity which is about 30% of its normal level.

What does this mean for shippers

Issues at these ports are causing further delays and restricting capacity in a fragile system. This is the case for not only spot rates, but also restricting allocations on the contract market.

It is no longer a certainty that all shipments will be able to move on contractual terms. Meanwhile, shippers should also be ready to alter shipping plans via alternative ports in the event of changed routes.

This will undoubtedly put upward pressure on rates. We have already seen prices of $15,000+ in the market. Shippers must be prepared to prioritise valuable cargo that remains profitable with these elevated rates.

Shippers should expect a ripple of congestion at the destination with a lag time of two to five weeks.

We are working closely with our customers and partners on sourcing alternative strategies around different shipping lines, different service levels and different port of departures. If you are a Zencargo customer, or simply in need of impartial, free advice, our supply chain teams are standing by to advise you on next steps.

Ocean

Asia → North America

Rates

Rates have increased by $500/40’ to US East Coast and $300/40’ to US West Coast.

Capacity

Port congestion at Yantian is affecting the services to the US.

HMM has announced 16 calls affected. There will be 12 calls cancelled and four calls diverted.

Ocean Alliance has 4 calls impacted that will either be diverted or cancelled

Equipment:

We are still facing chassis shortages. A good indicator is the operational update received from Hapag Lloyd which summarises the trend observed in the market.

Minneapolis, Indianapolis – Constrained on 40’ chassis..

Chicago, Detroit, Memphis, Seattle, Tacoma – Deficit on 40’ chassis.

Denver – Constrained on 40’ chassis. Units going direct to ground.

Los Angeles / Long Beach – Deficit on 20’/40’ chassis.

Ports

No improvement with one-two weeks average waiting time to berth in Los Angeles/Long Beach and three weeks in Oakland. Given the congestion now at Oakland, Hapag is omitting calls between Week 26 and 33.

Asia → Europe (Far East Westbound)

Rates

Rates being released now by some carriers indicate the trend of an increase of $1000/40’. It is expected the rest of the carriers will follow.

Capacity

The impact of the Yantian congestion continues to limit the amount of space available in the market as carriers omit calls:

Ocean Alliance (OOCL, COSCO, CMA, Evergreen) has eight calls impacted that were announced. There will be three cancellations, four calls diverted to Nansha and one to Shekou.

2M Alliance has 11 calls being affected. There will be two calls diverted to Nansha and nine calls will suffer a delay but will still call at Yantian.

THE Alliance (HMM, ONE, Hapag, Yang Ming) has 12 calls affected. There will be four calls cancelled, four calls diverted to Nansha and four calls delayed yet still calling at Yantian.

Equipment

Severe shortage of 40’HC equipment continues with no improvement from Maersk, ONE, ZIM, Evergreen, CMA and Yang Ming. HMM, MSC, COSCO and Hapag have improved availability in one extra port. The limited pockets of stock available include:

Shanghai (ONE, HMM, MSC, OOCL, Hapag)

Yantian (HMM, MSC, COSCO)

Shekou (COSCO)

Ningbo (OOCL).

The 40’GP stock is more available with options in:

Shanghai (Hapag, ONE, MSC, OOCL, COSCO)

Nanjing (Maersk)

Xiamen (Maersk)

Nansha (Maersk)

Hong Kong (Maersk)

Shantou (Maersk)

Ningbo (MSC, Evergreen, OOCL, COSCO)

Shekou (Evergreen, COSCO)

Xingang (COSCO).

Ports

Yantian is working at 20% productivity which is now putting pressure in the surrounding ports of Shekou which has announced heavy cargo acceptance restrictions to cope with congestion.

The port of Nansha is now congested with trucks having to queue for 8 to 9h to get through the terminal gates.

The rest of the main ports in China have not reported congestion yet.

Europe → USA (Transatlantic Westbound)

Rates

Rates released for June indicate an increase of $500/40’ of Equipment imbalance and another $500/40’ of Peak Surcharge. No further increases have been announced.

Capacity:

Space is fully booked from now until the end of June.

Equipment:

There has been no improvement in the shortage of chassis available last week.

Ports

No improvement in the inland operations from the ports. Vessel operations however remain with congestion.

Air

Airfreight rates cooled as the month of May progressed but this is unlikely to signify the start of a return to pre-Covid levels.

Writing in the Baltic Exchange market round up, Bruce Chan, vice president of global logistics at investment bank Stifel, said this downward trend as the month progressed was unlikely to signify a return to pre-Covid levels. He said that belly capacity on international flights remained depressed due to the slow roll out of vaccination programmes and the emergence of new variants. Meanwhile, demand continues to be brisk even heading into the summer lull as consumption remains high, inventories are low and there is ongoing supply chain disruption.

Asia

US market

Increase in demand ex PVG into North America, in particular, IT equipment and vaccine. The influx in demand means there is restricted space this week. Rates floating between $9.00-$10.00/kg.

Rates ex North China (TSN/PEK) and South China (CAN/SZX) remain the same this week between $8.00-$10.00/kg.

For all airports – rates and space must be checked on a case by case basis.

EU market (base airport like FRA/AMS/LUX, etc)

Market out of PVG into Europe is not as hot this week but due to flight cancellations rates have not decreased by much. We are looking at rates between $5-6/kg.

Rates and space must be checked on a case by case basis.

Spot rates available for heavy/dense cargo as well as volume cargo.

UK market

No significant change. Rates remain the same.

There are direct flights with CA/BA, AIR-AIR by SQ and normal air-truck service. Space using deferred carriers is fully booked.

Rates and space must be checked on a case by case basis.

Spot rates available for heavy/dense cargo as well as volume cargo.

Americas

For more than a decade, 100% of shipments departing from the USA on a passenger aircraft were to be screened by either a Certified Cargo Screening Facility (CCSF) or by the airline itself. Shipments departing on an All-Cargo/Freighter aircraft were excluded, but not anymore, as of July 1st 2021, all shipments must be screened. That includes cargo on carriers such as DHL, Fedex, CargoLux, UPS and any other freighter airline.

Cargo moving on a passenger aircraft is limited by size to what can fit below the passenger deck of an aircraft, and thereby making the task rather manageable. You cannot fit a large piece through an x-ray machine nor hand search a large engine. It will certainly take some time getting used to the new regulations by the industry at large. Many airline terminals and General Handling Agents are very busy as it is. Adding the screening task is certain to create delays until everybody in the supply chain is familiarised with the new regulations.

No real change from last week. Demand in several markets continues to outstrip supply as eCommerce traffic increases and economic activity strengthens in many markets

Forwarders continue to move greater volumes to secondary, smaller airports to avoid ground handling bottlenecks at main air cargo gateways. Airports such as LAX and ORD are being overwhelmed by surging demand caused by large import volumes and increased freighter traffic from Asia and Europe.

Delays expected are anything between 2 – 7 days.

Europe

Global freighter capacity is “maxed out” for 2021 and 2022 and with continued COVID-19 outbreaks and travel restrictions likely to remain in place, it is unclear how much passenger orientated belly capacity can be added through 2021 as countries struggle to curb the impact of the pandemic.

The freighters that are flying, are operating to maximum block hours and every available freighter aircraft has been put into service, which has enabled maindeck capacity to increase by 30% when compared to pre-COVID levels. But belly capacity, which prior to the health crisis represented 55% of all air cargo capacity, is still down by slightly over 50%, with an overall capacity shortfall of around 25%.

With demand outstripping capacity, flights are full across the board, on pretty much all trade lanes and current market conditions are likely to continue through June, based on large amounts of cargo in the pipeline.

European export demand stays strong to the Americas and Asia and space to USWC remains constrained.

Space to India and Bangladesh is very constrained, due to aid and relief shipments into the COVID-struck region.

Major airport hubs, as well as secondary gateways in Europe are reporting normal throughput for air imports and air exports, despite the significant reduction in passenger flights arriving and departing from the region.

Road

Availability

Availability generally reliable, though some issues remain with capacity from Italy. Reefer trucks are becoming more in demand as temperatures rise.

Rates

Rates remain stable across consolidated, groupage and dedicated trailers.

Customs

Border situations have improved considerably, with most crossings clearing on the same day as border staff and shippers improve compliance with post-Brexit regulations.

The route ahead

The information that is available in the Weekly Market Update comes from a variety of online sources, partners and our own teams. Click below to learn more about how Zencargo can help make your supply chain your competitive advantage.